Industry News

- Coated Freesheet Mill West Linn Complete Closure

- October 16th announcement and immediate closure related to loss of pulp supply and exposure to higher market pulp prices

- 3 PM’s total 270,000 tons/year;7% of North American supply

- http://westlinnpaper.com/announcement.html

- UPM Announces Shut of PM5 at Blandin Mill in Q1 2018

- Produces 128,000 tpy of coated groundwood, 5% of North American supply

- Affected business to be transitioned other PM’s in UPM system

- https://www.upmpaper.com/whats-new/

- Verso Announces Formation of Strategic Alternatives Committee

- Committee will identify and evaluate strategic transactions including the possible sale of some Verso mills

- NORPAC Trade Case Against Canadian Producers of Uncoated Groundwood Publication Grades Proceeds

- US ITC found merit to dumping (ADD) and government support (CVD) claims against Canadian producers (Resolute, Kruger, Catalyst, White Birch) and referred case to Department of Commerce for further review

- After request for delay, CVD determination now scheduled for 1/8/18, ADD determination now scheduled for 1/16/18

- Georgia Pacific Closing Uncoated Freesheet PM in WA

- Cut-size and offset PM at Camas, WA to close in Q2 2018

- UPM Signs Deal for Potential New Pulp Mill in Uruguay

- Two-billion-euro project could scale up to produce two million tons annually of eucalyptus pulp

Publication Paper Pricing – Historical View 2010 – 2017

| In light of the recent price increases in publication grades of paper here are the high and low prices for benchmark grades from the RISI Paper Trader since 2010 (post Great Recession) to give context. |

| Grade |

High |

Period |

Low |

Period |

Current |

| 50# Offset |

$47.50 |

Jul 2011 |

$41.75 |

Jul-Sep 2017 |

$42.25 |

| 60# #3 |

$50.50 |

Jul-Nov 2011 |

$41.75 |

Mar-Jun 2017 |

$43.50 |

| 40# #5 |

$46.25 |

Aug-Sep 2011 |

$36.75 |

Feb-Mar 2010 |

$38.75 |

| 35# SCA |

$42.50 |

Aug-Nov 2011 |

$35.25 |

Jan-Sep 2017 |

$36.00 |

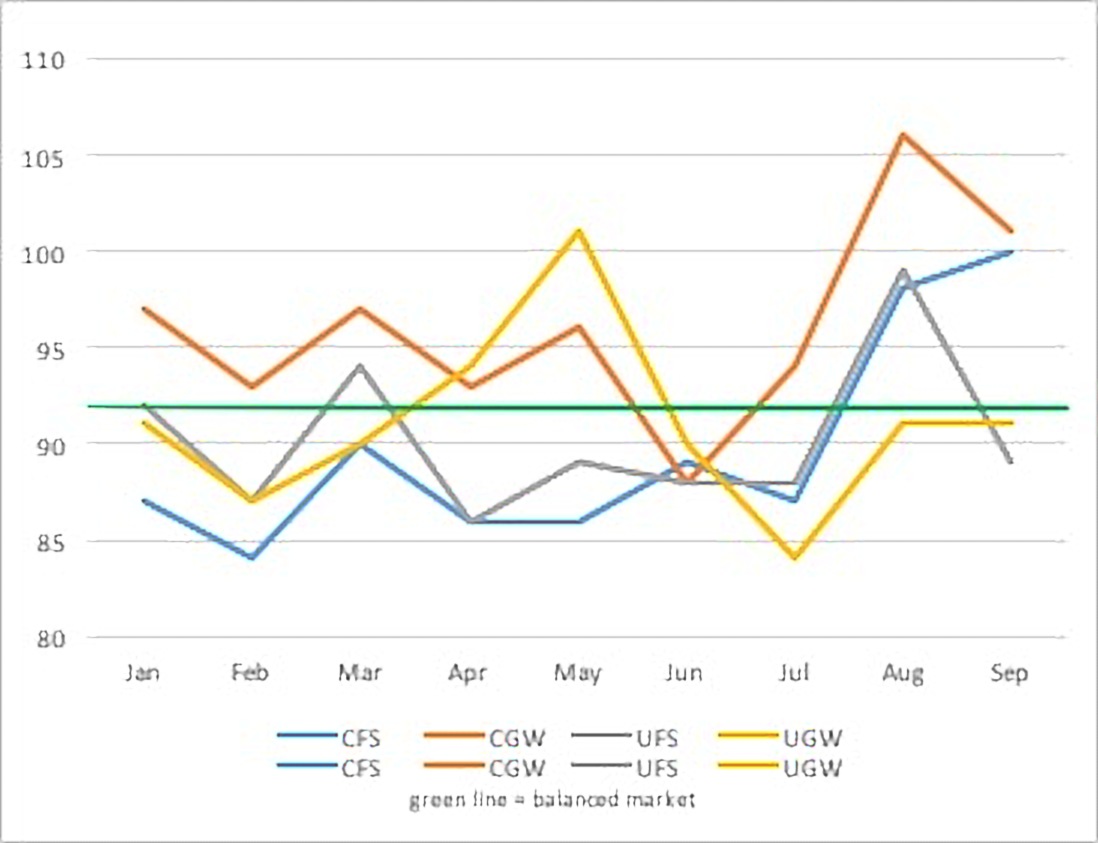

Mill Operating Rates (shipments to capacity - not seasonally adjusted)

Product Segment Commentary

- Coated Freesheet

-Q4 operating rates in high 90’s due to seasonal demand and loss of West Linn, Appleton Coated (14% of N.A. supply)

- Lead times as much as 8 – 10 weeks

- Near to mid-term forecast is for mills to operate at or close to full capacity

- SAPPI conversion project at Skowhegan mill will remove 30 days of production from 1 of 3 paper machines in Q1 2018

- Mill inventories are low with little time near term to restock

- Demand decline moderating at less than 5%/year loss

- $2.00/cwt price increases announced for November 1

- Coated Groundwood

-Q4 operating rates in high 90’s to over 100 due to seasonal demand and July capacity loss (Resolute’s PM2 at Catawba)

- Lead times 4 – 8 weeks

- Demand decline continues close to double digits/year

- UPM PM5 closure will keep remaining capacity busier in H1 2018 than historical averages

- Uncoated Freesheet

-After one-month blip in August to 99% operating rates fell back to yearly average of 89-90%

- Capacity loss in process due to closure or repurposing coated freesheet capacity back to coated grades

- PCA converting 1PM in Q2 2018; GP closing 1PM in Q2 2018; IP converting 1PM in 2019

- Decreased supply to West Coast coming in 2018 could require longer lead times and/or freight considerations

- Suppliers continue to balance supply and demand to help manage prices

- Uncoated Groundwood

-High bright ground grades lead times 4 – 8 weeks in part due to loss of capacity in Q3 2017

- SC grades continue to suffer due to loss of retail advertising

- Newsprint capacity closures resulting in high operating rates and higher prices for near to mid-term

- Cloud of unfair trade case hanging over Canadian producers of newsprint/high brights which could result in price increases or mill closures if duties are imposed

Send us a message

To get in touch with us, fill out the form below and we will reach out to you as soon as possible.

Required fields are marked with a (*).